There is virtually nowhere on the Internet you can go today without encountering some form of Generative AI. There is virtually nowhere in the workspace you can go either, with Generative AI dominating conversations from the board to the break room.

A March 2023 KPMG survey of U.S. executives found that almost two-thirds (65%) believe “generative AI will have a high or extremely high impact on their organization in the next three to five years.”

The catch? “Fewer than half of respondents say they have the right technology, talent, and governance to implement generative AI successfully.”

This finding may surprise those who encounter chatbots and read AI generated content daily. But for those of us who’ve been tracking the corporate digital transformation journey, and mapping it against the six technical capabilities required to successfully navigate that journey, we aren’t surprised at all.

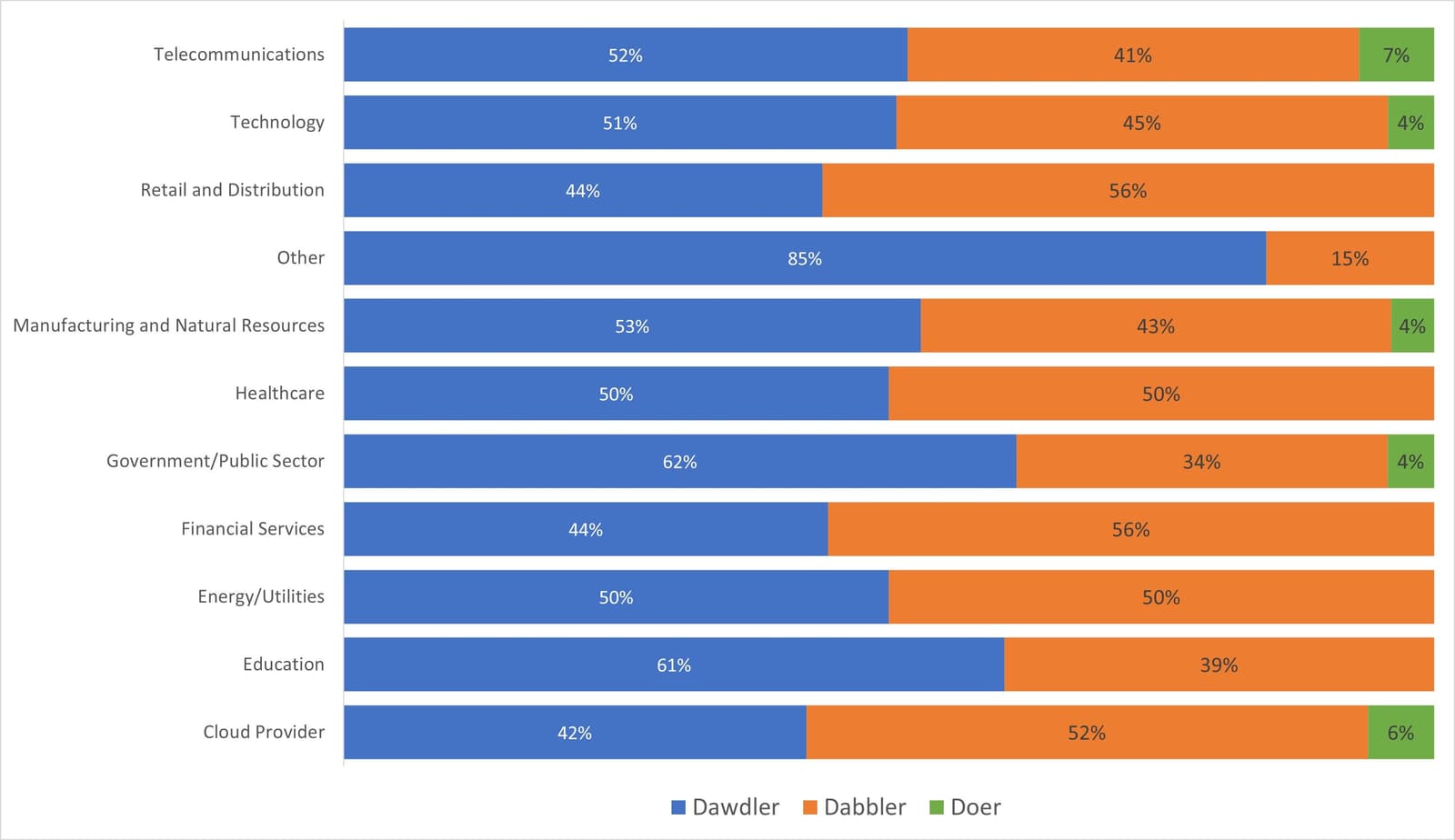

We did a deep dive into the current state of digital enterprise maturity based on those six technical capabilities and found only 4% of the organizations operating at the highest level of maturity. That is, they are close to fully operating as a digital business.

Most organizations (65%) are dabbling in digital business. They show signs of maturity, harvesting the rewards of the hard work of modernizing IT and its technology domains. Notably, this is nearly the same percentage KPMG found lamenting a lack of the right technology, talent, and governance to implement generative AI successfully.

That’s not a coincidence. The sheer breadth and depth of technical capabilities required to establish and operate an AI-enabled business can be overwhelming. From new technical domains in the enterprise architecture—SRE operations, observability and automation, app delivery, and security—to modernizing existing domains such as data and infrastructure, a significant amount of work is needed, especially for enterprises that predate the Internet.

That’s why it’s no surprise that when we look at the maturity of organizations through the lens of industries, we find that no financial services organization is operating at the highest level of maturity. Cloud providers, telecom, and technology firms dominate that category. With the exception of telecom, cloud providers and technology firms are relatively adolescent industries with very little technical and architectural debt than their more-traditional counterparts. That makes it a lot easier for them to push forward faster.

The lack of Financial Services companies in the highest category of digital maturity—the doers—might seem odd given the rapid rise of digital banking. Upon deeper analysis, one can assume that FinServ is moving at a slower rate by design. Adding a new interface (apps and digital services) is much like putting a shiny façade on an old building—it gives the appearance of modernization but behind the scenes is a great deal of traditional technology and practices. That’s not a condemnation. After all, there are costly risks to missteps, and they have a considerable burden with existing infrastructure and app portfolios requiring modernization.

This also explains the lack of healthcare companies in the top category. If a weighty portfolio and strict governance burden the financial services industry, imagine the burden on healthcare organizations. Their tendency to move at a much slower rate than other industries is understandable. They are one of the most highly regulated and tightly governed industries, and rightly so, since missteps impact human lives. Digital transformation is not a race; thus, it is encouraging to see some industries progressing with a measured, strategic approach. The tortoise did beat the hare, after all.

That’s not to say there aren’t examples of healthcare and financial services that are progressing faster than others. The data set we analyzed was drawn from responses to our State of App Strategy survey, based on the completeness of answers. Companies we’ve spoken to in both industries have demonstrated that there are exceptions to every statistic.

Specific factors force the adoption of new technology earlier among certain industries that would otherwise be inclined to be more cautious.

Healthcare

The healthcare sector, for example, needs more critical care nurses to cover the number of available hospital beds. This shortage of resources is an existential threat but entirely outside of the control of the industry because there just are not enough nurses to go around.

To meet this challenge, some healthcare providers—especially those managing a large number of hospitals—are increasingly looking at how Artificial Intelligence can increase the number of beds each nurse can cover without compromising the quality of care. Some providers are looking to Large Language Model AI to make nurses more effective by reducing the time needed to maintain patient health records. Others intend to use AI visual modeling to monitor hundreds of high-definition video streams for possible changes in patient conditions (e.g., labored breathing, poor skin pallor, or patients who have fallen). But because the standard of care requires near-real-time reactivity, the most effective applications being developed for this purpose are Edge applications with sophisticated uses of records analysis and computer vision assessment—a far cry from the healthcare applications based on rather ancient systems and standards.

Financial Services

Financial Services companies can sometimes lag in their adoption of certain technologies because they’re generally highly regulated. But bankers and brokers know that the greater the risk, the greater the reward. Using applied technology to obtain a first-movers advantage over competitors is central to the Financial Services industry embracing blockchain despite significant difficulties with reliable deployment, considerable risk, and regulatory scrutiny.

The early academic studies in Quantum Computing exemplify how far beyond regulatory structures the Financial Services industry is willing to go for an advantage. The industry has forecast certain advantages from the technology and is bankrolling some of the most sophisticated studies in areas such as Quantum Key Distribution, which can significantly increase the efficacy of security around transaction processing for monetary transfers or trading.

Manufacturing

What typically surprises people is the presence of manufacturing companies in the “doers” category. The 2022 SOAS found that IT/OT was the most exciting technology trend, and it remained in the top five in 2023, demonstrating that manufacturers are at the forefront of modernization.

Manufacturers have always been on the vanguard of adopting any technology that leads to greater efficiencies—it was not banks that adopted and optimized the assembly line, after all—and digitization is no exception. The annual Oil and Gas Automation Conference for the past three years has shown that natural resources sector is far ahead of most enterprises in their use of automation, collection of telemetry, and the adoption of Zero Trust approaches to securing remote assets.

Get On Board or Get Left Behind

The benefits of the digital transformation journey are undeniable. Organizations in all stages of digital transformation see benefits, and those exhibiting greater maturity are more likely to cite business benefits such as competitive advantage, new opportunities, and business operational efficiency.

There are very few technology trends that impact every organization in every industry. Generative AI is just one of many disruptive technologies ahead, and if organizations can’t harness these game-changing technologies, they will undoubtedly be left behind. Digital maturity indicates whether or not an organization is well-positioned to take advantage of these technologies.

Download the full report for a deeper dive into the Digital Enterprise Maturity Indexand the practices and habits of Doers, including the use of public cloud, automation, and security practices.

About the Author

Lori MacVittie is a Distinguished Engineer and Chief Evangelist in F5’s Office of the CTO with deep expertise in application delivery, automation strategy, and infrastructure. She is known for turning complexity into clarity whether she’s defining guardrails for AI agents, dissecting brittle multicloud architectures, or probing the limits of scalable systems. She brings more than thirty years of industry experience across application development, IT architecture, and network and systems operations. Before joining F5, she served as an award-winning technology editor. MacVittie holds an M.S. in Computer Science and is a prolific author whose publications span security, cloud, and enterprise architecture. She is also an avid tabletop and video gamer with unapologetically strong opinions about cheese.

More blogs by Lori Mac VittieRelated Blog Posts

Multicloud chaos ends at the Equinix Edge with F5 Distributed Cloud CE

Simplify multicloud security with Equinix and F5 Distributed Cloud CE. Centralize your perimeter, reduce costs, and enhance performance with edge-driven WAAP.

At the Intersection of Operational Data and Generative AI

Help your organization understand the impact of generative AI (GenAI) on its operational data practices, and learn how to better align GenAI technology adoption timelines with existing budgets, practices, and cultures.

Using AI for IT Automation Security

Learn how artificial intelligence and machine learning aid in mitigating cybersecurity threats to your IT automation processes.

Most Exciting Tech Trend in 2022: IT/OT Convergence

The line between operation and digital systems continues to blur as homes and businesses increase their reliance on connected devices, accelerating the convergence of IT and OT. While this trend of integration brings excitement, it also presents its own challenges and concerns to be considered.

Adaptive Applications are Data-Driven

There's a big difference between knowing something's wrong and knowing what to do about it. Only after monitoring the right elements can we discern the health of a user experience, deriving from the analysis of those measurements the relationships and patterns that can be inferred. Ultimately, the automation that will give rise to truly adaptive applications is based on measurements and our understanding of them.

Inserting App Services into Shifting App Architectures

Application architectures have evolved several times since the early days of computing, and it is no longer optimal to rely solely on a single, known data path to insert application services. Furthermore, because many of the emerging data paths are not as suitable for a proxy-based platform, we must look to the other potential points of insertion possible to scale and secure modern applications.